Do you know your tax bracket?

I’d say a good number of people do.

But do you know what happens when you jump up to a new tax bracket?

I’d say a good number of people do not.

Tax season is over (unless you pressed the IRS snooze alarm filed an extension), but as your income can change all the time, it’s never a bad time to understand what exactly how tax brackets work.

And if you think it’s a boring topic, I would urge you to reconsider. Anything that has the ability to lop off a significant portion off each and every paycheck you get is probably worth your while to understand, right? Right.

Taxation 101

As a recap, when you earn a wage, you get taxed on it.

(As a further recap, taxes are the thing that enables our country to keep the lights on. So while everyone, myself included, wants to pay less taxes, we need to remember that the less tax we pay, the less services we all receive.)

Anyway, the rate of tax that you pay is dependent of how much you make. This system is called a “progressive” tax system because the more you make, the higher your rate.

And this is where the idea of “tax brackets” come in.

As of the time of writing, these are the tax brackets for a single person:

[table caption=”Tax Brackets, Single, 2017″ width=300]

Tax rate, Income threshold

10%,$0 to $9325

15%,$9325 to $37950

25%,$37950 to $91900

28%,$91900 to $191650

33%,$191650 to $416700

35%,$416700 to $418400

39.6%,$418400+

[/table]

Those who file as married or head of household have slightly different income ranges for the tax brackets, but the general idea is the same:

[table caption=”Tax Brackets, Married Filing Jointly, 2017″ width=300]

Tax rate, Income threshold

10%,$0 to $18650

15%,$18650 to $75900

25%,$75900 to $153100

28%,$153100 to $233350

33%,$233350 to $416700

35%,$416700 to $470700

39.6%,$470700+

[/table]

[table caption=”Tax brackets, Head of Household, 2017″ width=300]

Tax rate, Income threshold

10%,$0 to $13350

15%,$13350 to $50800

25%,$50800 to $131200

28%,$131200 to $212500

33%,$212500 to $416700

35%,$416700 to $444500

39.6%,$444500+

[/table]

Learn more about these tax brackets.

If you want to understand the current U.S. political climate, this is approximately what those in power want to do if they could:

[table caption=”Please let this not happen” width=300]

Tax rate, Income threshold

15%,$0 to $9325

20%,$9325 to $37950

30%,$37950 to $91900

25%,$91900 to $191650

10%,$191650 to $416700

5%,$416700 to $418400

0%,$418400+

[/table]

Back to reality, let’s keep in mind that this is just federal tax brackets. Your state has their own tax brackets that are entirely different, and add to your total tax due. For example, in Oregon, where I live, the tax rates are between 5% and 9.9%.

Mo’ money, mo’ brackets

It turns out that while we all read the same table, we don’t interpret it the same way.

This is why you hear people say things like:

“I don’t want to do that, since it will put me in a different tax bracket.”

“If you cash out your retirement too soon, you’ll be in a higher tax bracket.”

“I want get as close as possible to the top of my tax bracket but not go over.”

If you’ve ever though these things, I’m happy to report that you are misinterpreting what a tax bracket is.

How tax brackets really work

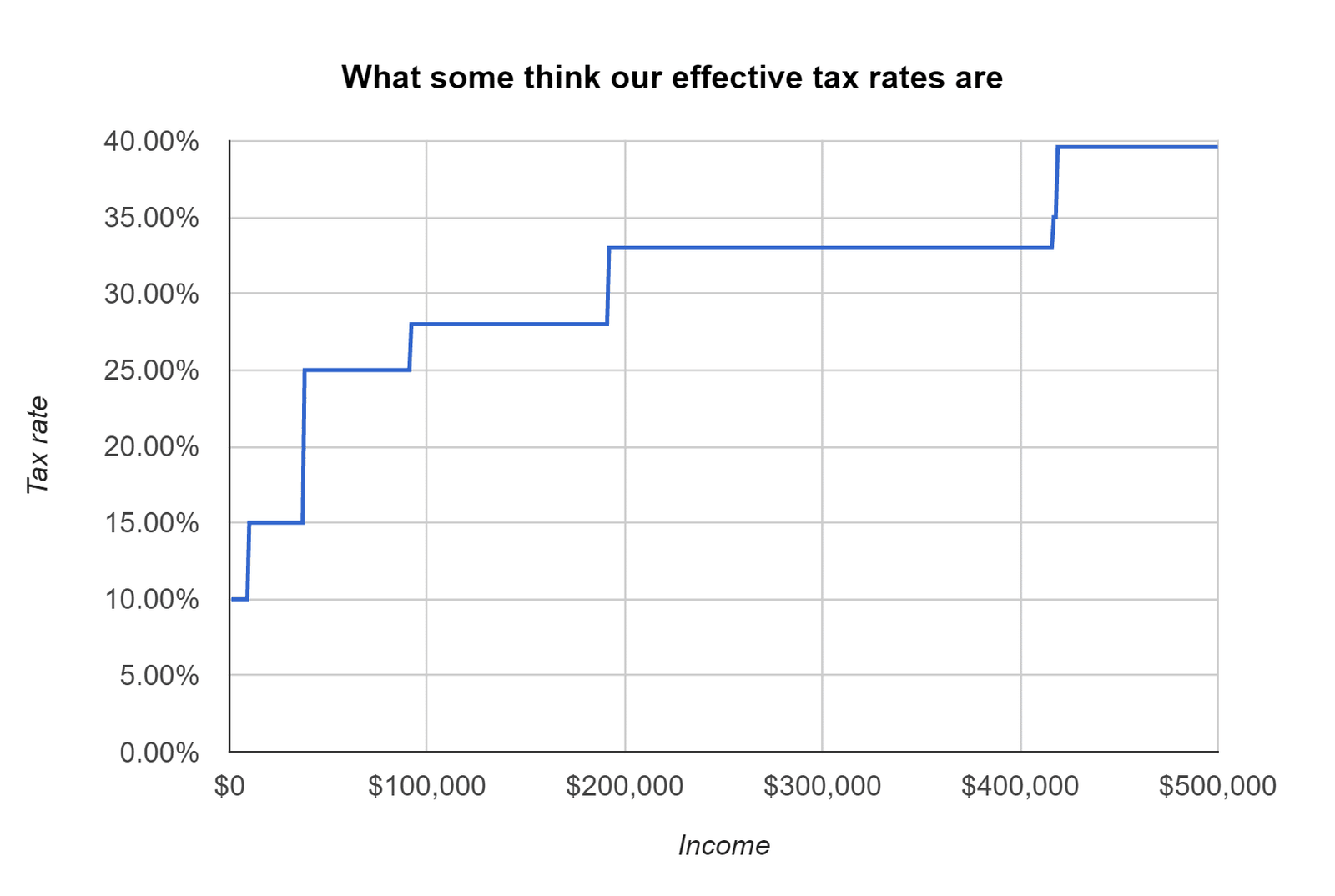

Here’s what some people think their tax looks like:

If I’m single and make $91,900, I’ll be taxed at 25%, but if I make $92,000, I’ll be taxed at 28%.

This is wrong.

These people look at tax brackets and see the following graph (for a single person):

But that’s not how it works. A the tax bracket refers to the tax rate paid on the income range, not the whole income.

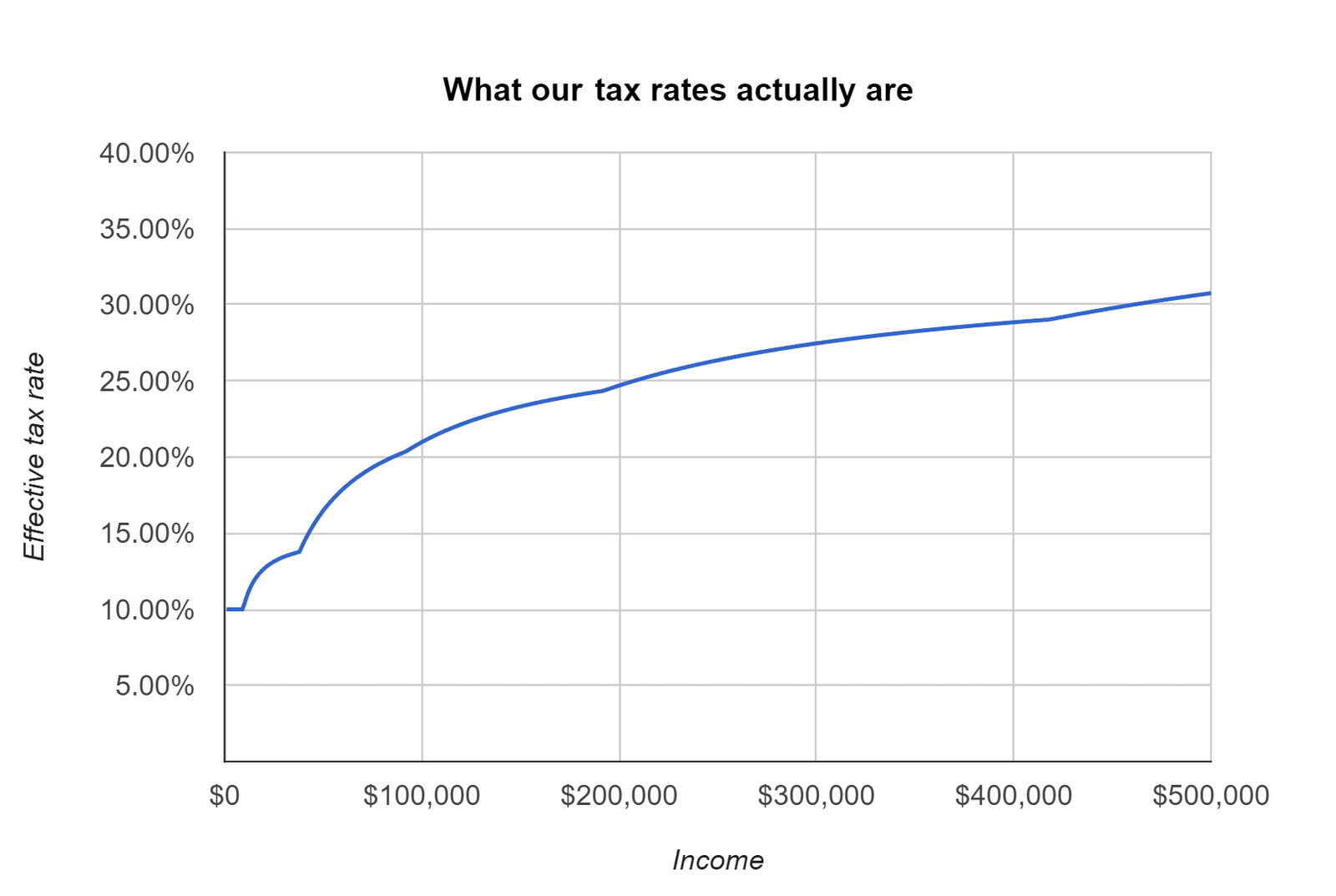

So, if you make $92,000 and you’re single, the following calculation occurs:

- You pay a 10% tax on the first $9,325

- You pay a 15% tax on the next $28,625

- You pay a 25% tax on the next $53,950

- You pay a 28% tax only on last $100

So the graph for our effective tax rates as a function of income actually looks like this:

(Important caveat: This has nothing to do with deductions. Deductions affect what actually counts as your income. Totally different thing.)

Notice how smooth the curve is. This means that there is no real marked effect when you move over to a new tax bracket. You’re not going to automatically be saddled with thousands of dollars in extra tax.

If that were not the case, there would be whole industries that exist to find a way to get one’s income to be at the very maximum of the tax bracket without going over. It would become a The Price Is Right kind of charade. It would be silly.

So if you’re worried about being bumped up to a higher tax bracket, breathe easy. Yes, the money above that threshold will get taxed at a higher rate, but only that money.

You should be more grateful that you got a raise in the first place.

Want to see the spreadsheet where I made all these calculations? Here you go.

Want to check my work against the IRS? Here is the IRS tax table worksheet.

2 Comments

AC

Good point. But it does make a difference if you’re married with kids the more money you make the less you get back by the end of the year when you file taxes. And you lose other benefits like Medicaid and so on

Mike @ Unlikely Radical

Hi AC. Thanks for weighing in. You’re quite right that income levels do affect eligibility for things like Medicaid, Roth IRAs, etc. And yes, the more money you make, the more taxes get taken out, though even still you’ll end up taking home more in the end.

My point here was that merely stepping over into the next tax bracket wasn’t going to trigger a giant financial event, which some people mistakenly believe is the case.