You might think that the life cycle of owning a home is that you buy something, get a mortgage, pay off mortgage, and then live happily ever after.

But this omits the fun world of mortgage refinance. Because it was so fun to go through the process of getting a mortgage once, you can go through that whole process again!

Jokes aside, is a mortgage refinance something you would want?

Why refi

A mortgage refinance is the process of getting a new mortgage to replace your existing mortgage.

One would refinance one’s mortgage to receive more favorable terms. Some more favorable reasons would be:

- A lower rate

- Moving from variable rate to fixed rate

There are other reasons, but most of those feel ill-advised to me, so I’m not going to talk about the here.

In a way, a mortgage refinance is kind of like of consolidating student loans, except in this case there is only one loan. With student loans, one refinances to get a lower rate and better terms too, but you need to have more than one of them to be able to qualify. But with a refinance, there is no such restriction.

So let’s look a bit at how those benefits shake out.

Lower rate

Who doesn’t want a lower rate on their debt?

Rates move around like that marble in that wooden labyrinth game. And while we don’t quite know where it is for us, we hear ads saying “mortgage rates are going down; lock in today!”

And it’s true that mortgage rates are some of the lowest that we have seen in my life time.

And a little rate change can make a significant difference over the life of the loan.

For example, a $200,000 mortgage on a 15 year plan at 5% is a total of $284,685, while at 4% it is only $266,287, a difference of $18,398. Not too shabby.

The higher your interest rate is, the more significant the 1% reduction is. Going from 8% to 7% in this case yields a savings of $20,458.

So a rate reduction is significant, but it comes with some caveats.

- The quicker you pay off your mortgage, the less you’ll be affected by interest rates.

- You might not get 1%.

So, as always, it’s important to actually calculate how much savings you’d receive.

Moving to fixed rate

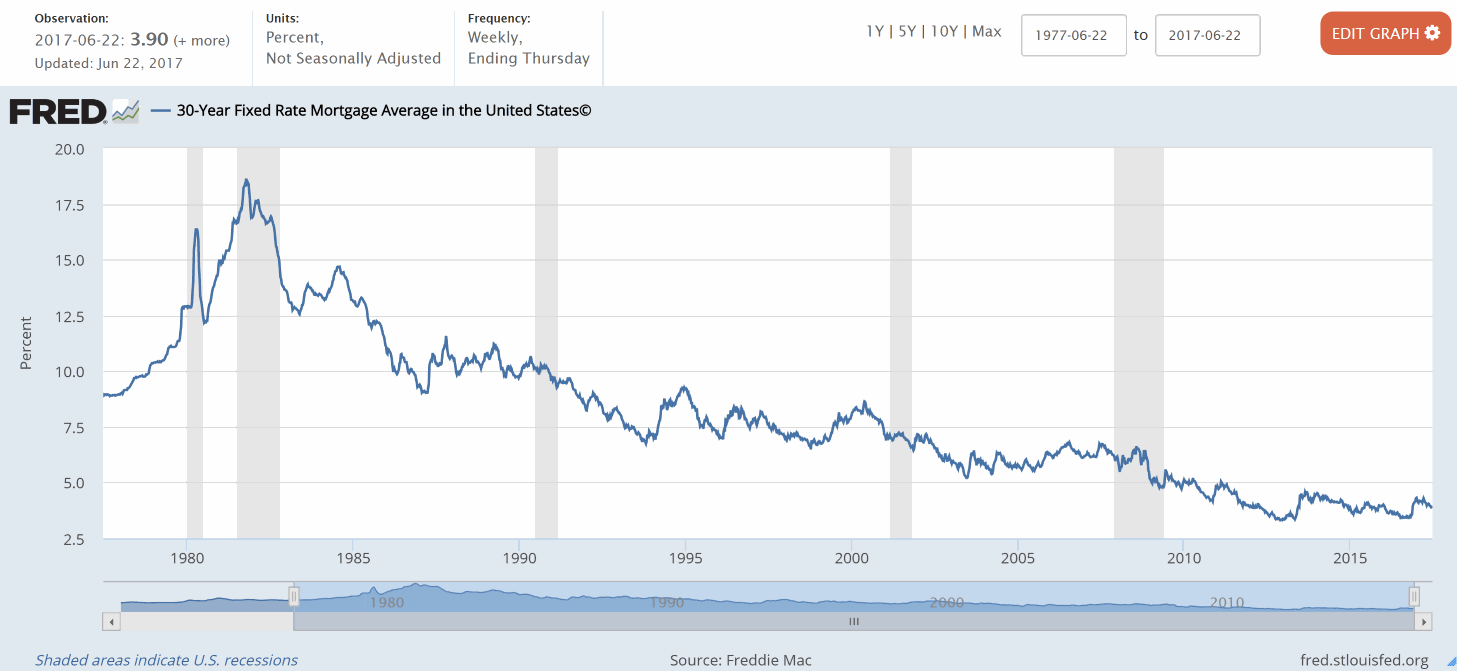

An Adjustable Rate Mortgage (or ARM) is one whose interest rate changes over time.

These are almost unequivocally bad news for anyone who’s getting into the game right now. The reasoning is easy: look at the graph above: do you think over time rates are likely to go higher or lower? And how much room is there for each direction? Rates can’t go much lower than they are now, but they’ve got a lot of room to rise.

And plus, a fixed rate allows you to plan. My mortgage bill is the same every month. It’ll be the same years from now.

Conversely, I once had a private student loan that was indexed to the prime rate. As rates rose (and rise they did), my payment went up every few months. It sucked.

So moving to a fixed rate is pretty much always a good plan here. Even if it’s a higher monthly payment for you right now comparatively, it may not always be that way. And predictability is important.

That said, again, it’s vital to actually calculate how much savings you’d receive.

Costs

“Nothing’s free in this world.” -My boss at the gas station, ca. 1997, on replacing the free air pump with one that cost $0.50.

Mortgage companies aren’t quite like your Internet Service Provider: you can’t just call them up and ask for a lower rate and then just get one. They will want to be paid for doing the work.

So you’re going to pay an upfront fee for the process of refinancing. This can run between $2,000-$5,000.

Let’s take a middle value of $3,000. Your savings needs to be more than that to make it worthwhile. Arguably, with all the hassle, it needs to be much more.

But I just quoted a savings of $20,000? Surely that’s a good deal then?

Maybe. But let’s see a more realistic example and see the monthly difference.

You have a 30 year, $250,000 mortgage, at 4%, which you’ve been paying on for 5 years. You now owe about $225,000. Your monthly payment is $1,193.

You then refinance to a 3%, 25 year loan. Your payment is now $1,067 per month, a savings of $126 per month.

In this scenario, it’s going to take you two years to break even on the deal. Only after that do you start saving a little bit of money.

Worth it?

It’s hard to calculate the true worth of a mortgage refinance. I personally think it’s only worth it if you’re gaining more than 1% in rate reduction, or if you’re moving from a variable rate to a fixed rate. Otherwise, it doesn’t seem worth the hassle. And a mortgage origination is a hassle, believe me.

Otherwise, I’ve got a plan that has you saving tens of thousands of dollars over the life of the loan: Commit to paying extra every month. Pretend your 30 year mortgage is a 20 or 15 year. Pretend your 15 year is a 10 year. Pretend like you don’t have a choice, that you are contractually bound to pay this off quickly.

The best part about this plan: no fees at all. You’re automatically approved.

But enough about me: Have you ever refinanced your mortgage?