Here in the US, we actually do have a small safety net for the elderly and disabled. It’s called Social Security (technically called “Old-age, Survivors, and Disability Insurance” or OASDI) The idea is that when you reach a certain age, or have a disaster/ailment befall you, you are eligible to receive a monthly stipend.

The benefits that you can receive from Social Security are not insubstantial, though not extravagant. The maximum you can receive per month is $3,350, though the average is more like $1,300.

I am a firm believer that Social Security is a good thing and should be there for us if and when we need it. I am happy to pay into it every month.

I also, perhaps contrarily, believe that you should not plan it for it to be there for you.

Insecurity

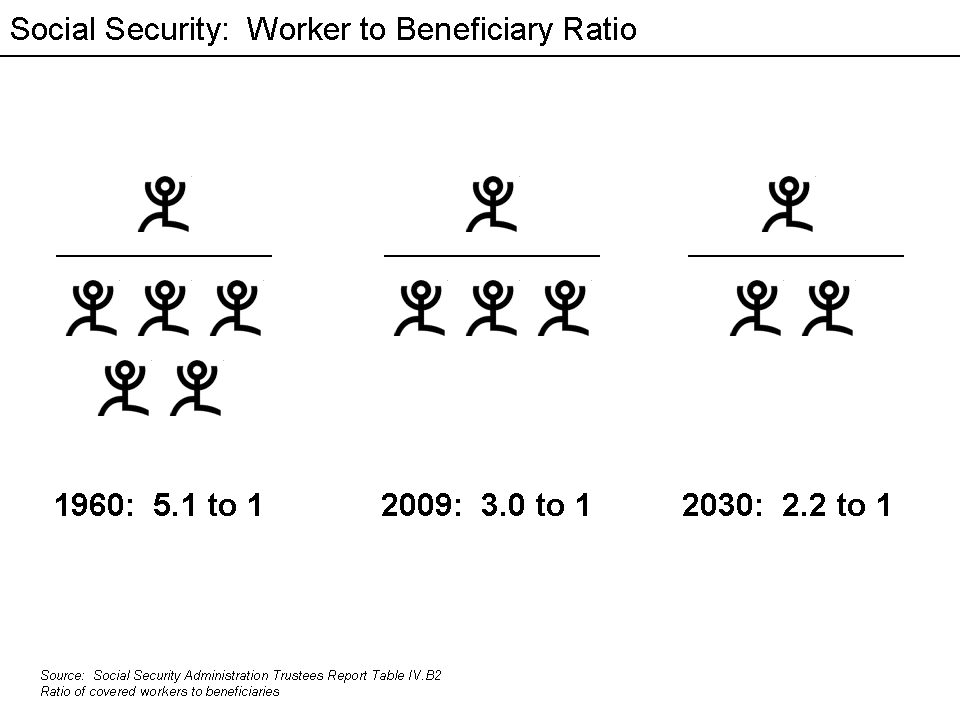

Pretty much any conversation about Social Security focuses on how it is unsustainable. Within some short timeframe (years or decades, depending on the source), it’s going to run out of money, causing calamity as it will be no longer able to pay out its promised benefits.

(Oddly, some say the solution to this is to cut the promised benefits now. Why this wouldn’t just force the same calamity sooner appears to be an unasked question.)

I don’t doubt that Social Security has fundamental structural problems. With the balance shifting from the number of workers paying into the system to the number of workers receiving benefits from the system, it’s simple mathematics that there will be funding problems.

(But again, I wonder why can’t just change the funding system to account for this.)

Anyway, all of the above isn’t really germane for our purposes here. Instead, you must ask: how does the current Social Security system affect you?

Walk your wire

The best way to plan your future financial life is to assume that Social Security will not be there.

Think of an wire walker in a circus. Yes, a wire walker knows that there is a net below that will be there should disaster fall (no pun intended). But that doesn’t mean that the walker plans to ditch the wire and fall onto the net. The net is only there as a backup. The wire walker must instead be competent enough to walk the entire wire.

The same goes for Social Security. Including Social Security in your financial planning is not unlike planning to ditch the wire.

Many of you are worried that you won’t have enough money for your retirement years. And this is a valid concern, and it’s why I think we all need to be investing experts.

But if you know that you have $1,300 a month coming to you when the time comes, your strategy will be different. You may not be as focused or as aggressive in your planning.

And in the spirit of that philosopher* who used a similar process for deciding whether or not to believe in the existence of God Pascal’s Wager, you really have four options:

- Plan for Social Security to be there, and it is (Result: Good)

- Plan for Social Security not to be there, and it isn’t (Result: Good)

- Plan for Social Security to be there, and it isn’t (Result: Bad!)

- Plan for Social Security not to be there, and it is (Result: Great!)

I don’t see a bad outcome if you plan for Social Security not to be there. And if you get to retirement age and there’s this extra money coming your way, then think of all the good things you could do with it.

I for one am thankful for what little safety net we have, although I don’t believe it’s nearly large enough for our current situation of stagnant wages and rising inequality. I don’t begrudge anyone for using the safety net should circumstances deem it necessary. But while we have the ability to do otherwise, let’s work toward that.

* I’m sure this was Descartes, but I can’t seem to find the source for it right now. Anyone know?

But enough about me. Do you plan for Social Security in your future?

{kind=link}

2 Comments

saulofhearts

Sounds like it might be Pascal’s wager?

Mike

Yes, that’s it! I updated the post. Thanks!