If you’re going to be financially comfortable in the later years of your life, you’re most like going to need to be a millionaire. Or if not an actual millionaire, derive the equivalent in income that having a financial net worth of a million dollars to net you.

(While I have a bias toward investment, I don’t discount things like income from real estate. It’s just not my particular thing.)

A million dollars isn’t a firm number. And recently, I’ve heard people saying that a million isn’t even enough today.

And there are those who have in their heads even larger figures, like even $10 million or more. Are they right?

Large numbers are hard

Let’s acknowledge that large numbers are hard to grasp. Can you really feel the difference between $1 million and $10 million? Between $10 million and $50 million? What about 100 million?

Because of this, I don’t feel like it’s a stretch to say that if someone feels like they need $10 or $50 or $100 million to retire, they probably haven’t actually run the numbers on what they need.

Lifestyles of the rich and insufferable

Let’s pretend that we have $100 million, and wanted to go on a shopping spree of the most grandest and epic proportions. (Let’s put aside that this would not make you appreciably happier, and would probably cause your life to be much more challenging.)

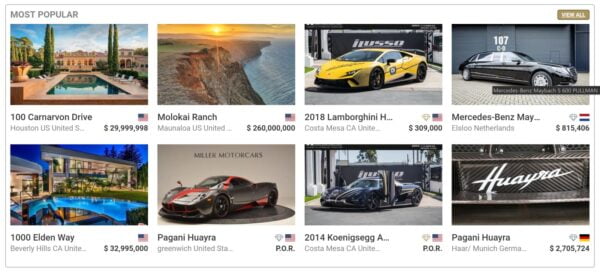

There’s a site called JamesEdition which is kind of like the eBay for the super rich. No Pez dispensers here. Look at what’s listed as “Most Popular”:

Okay, now put aside that this level of ostentatiousness is suspect. We’re going shopping.

Pretend you want a really nice house. I mean really nice. Like $32,995,000 nice. That would net you the above one in Beverly Hills.

Now pretend you want the nicest car you can find. You could get a Pagani Huayra for $2,705,724. (I had to look up that this was in fact a car; I’m so bad at this.)

But you can’t just drive around everywhere; you’re going to need a private jet. According to Bankrate, a private jet costs between $3 and $90 million. Let’s opt for a middle ground and go with $30 million.

What about your lifestyle? Luckily, with these three purchases, if you have, say, $100 million, you’re going to have around $35 million left over. At 6% interest, that would net you an interest income of $2 million a year.

A little closer to reality

Okay, that’s enough fun. We can easily move our decimal points a notch to bring us closer to reality. A $3 million home, a $270,000 car. (Closer to reality I said, not actual reality.) But with $3.5 million in the bank, earning 6% interest, that’s still earning you $200,000 a year.

Turning it around, if you want to earn in the ballpark of $200,000 a year in retirement, then you’re going to need about $3.5 million in the bank. And that’s a conservative estimate. With 8% interest, you would need about $800,000 less.

But do you really need $200,000 a year to live on comfortably? Are you living on that today?

Of course not. If you had $10 million in the bank, that would be great, but that would allow you to live a lifestyle that most people would only dream of. You should strive for that number if you want, but that’s clearly above and beyond what you would need.

Retirement does not mean rich

I think the confusion arises from the notion that when people get to retirement, they’ll magically be able to do everything they’ve ever wanted. And while that would be nice, and can certainly be possible, it’s not the star that I want us sailing toward. Why not? Because as much as I like setting ambitious goals, I much prefer goals that are achievable.

You’re not going to stop working one day and be magically able to everything you’ve ever dreamed of. You’re still going to need to have a money plan, figure out how much is incoming and how much is outgoing. And even though compound interest is an amazing thing, it’s unlikely that your lifestyle is going to hugely increase in retirement. It can get better, sure, more comfortable, more resilient.

Our goal is to be okay, fundamentally okay, safe, secure, at peace, resilient, comfortable. I believe that pretty much everyone can do that with diligence and patience. You don’t need $100 million for that. And it’s something you just can’t buy on JamesEdition.com.