In 2006, Congress passed the Pension Protection Act. It’s a scintillating read.

Among much else, it provided statutory authority for employers to enroll workers in retirement plans automatically, and also established criteria of “safe harbor investments” to protect employers from liability that comes from automatically enrolling employees.

Prior to this, people weren’t automatically enrolling in their workplace retirement plan, and Congress, in a rare moment of caring about working folks, decided that it was best for everyone to have an “opt-out” plan as opposed to an “opt-in” plan. If people were going to be lazy, let them be lazy in a way that benefits them.

But you can’t just put someone’s money just anywhere. (Enron stock?) So the bill establishes the idea of a Qualified Default Investment Alternative (QDIA) as a vetted fund that employers could be protected from liability if they used.

And target date funds were just such a plan.

Target date funds

Target date funds are investments that adjust their investment objective over time. Starting out aggressive, they become more conservative (less risk, less return) over time, tied to a particular date in the future.

The goal of these funds (sometimes called “lifecycle funds”) is to automate the allocation strategy that many (most?) suggest investors pursue: be aggressive in your younger years, and grow more conservative as you approach retirement. This way you maximize your returns when you can most afford risk, and then minimize risk when you can least afford it.

Basically every major investment firm offers some form of target date funds now.

But is it for you?

The funds

If you want to invest in target date funds, it’s easy to do, though every firm calls it something slightly different.

- Vanguard: Target Retirement Funds

- Fidelity: Fidelity Freedom Funds

- Schwab: Target Date Funds

- T. Rowe Price: Retirement Funds and Target Funds

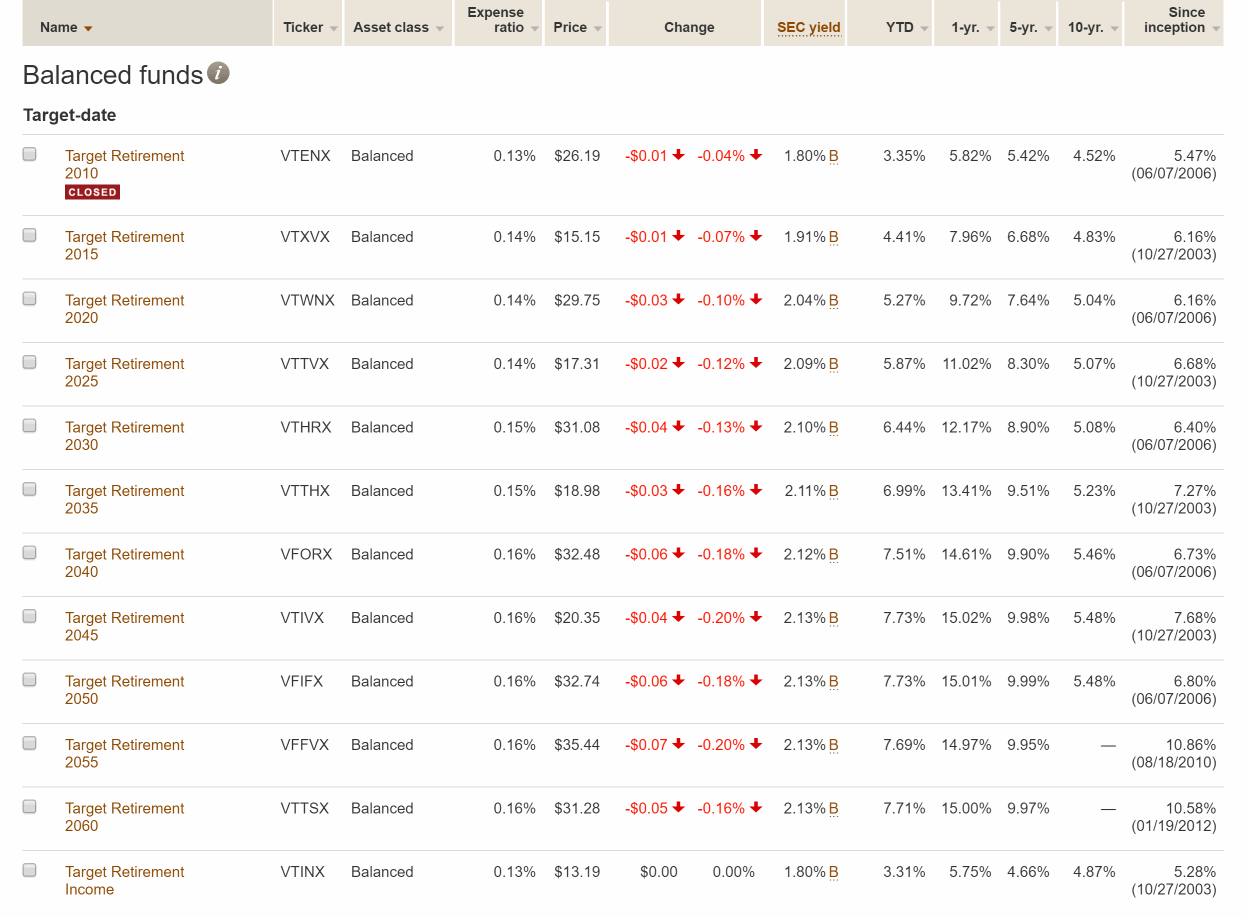

In the case of Vanguard, they have funds called “Target Retirement XXXX”, where XXXX is the target date of retirement.

They have a little utility to keep you from having to do any math, where they ask your age and tell you what fund is right for you. In my case, given my age, they recommended Vanguard Target Retirement 2045 Fund (VTIVX).

Fund’s progress

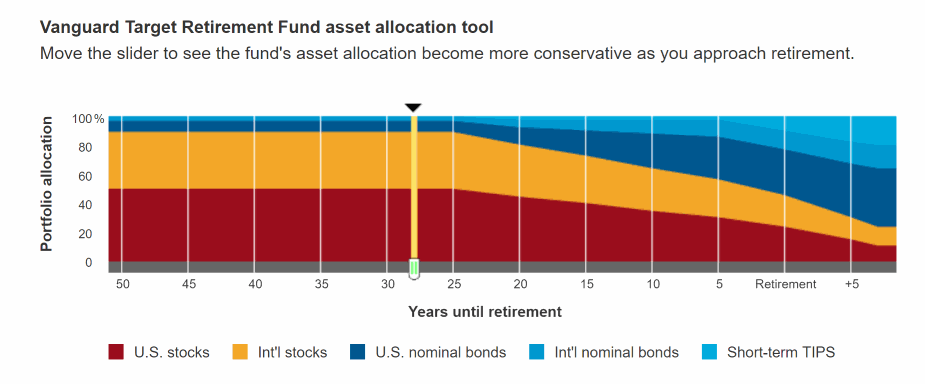

Vanguard helpfully shows an interactive graph showing the mix of stocks, bonds, and other assets over time, from now to the time of retirement. This can most effectively show what the plan is for this fund:

So right now, the allocation is:

- 54% U.S. stocks

- 36% International stocks

- 7% U.S. bonds

- 3% International bonds

However, this will change over time, and at the date of “my retirement” in 2045, the mix will be:

- 30% U.S. stocks

- 20% International stocks

- 30% U.S. bonds

- 13% International bonds

- 7% Short term TIPS (Treasury Inflation Protected Securities, basically investments that only track inflation)

Indeed, that is quite conservative.

So now that you know what a target date fund is, let’s talk about whether it’s a good idea for you.

Pros

- Easiest investment portfolio there is. These funds not only come with built-in diversification, but that also rebalance over time. For this reason, it is best for those who don’t wish to spend even the most minimal time thinking about their portfolio. Just set and forget.

- Can have lower minimums that other funds. In Vanguards case at least, the minimum to invest in a target date fund is $1,000, compared to $3,000 for most of their funds. As $1,000 is the minimum you need to invest, this could be a could place to get started.

- Lower risk. The focus on always having bonds in the fund, increasing over time, means that this is a fund focused on risk aversion.

Problems

- Long term track record not established. Target date funds were only invented in the 1990s, so they have no real long term track record. The oldest of the Vanguard funds was started in 2003. Considering the Vanguard 500 fund has a track record going back to 1978, that’s a pretty big difference.

- Lower returns. This shouldn’t surprise anyone, but due to the focus on lower risk, the returns are lower too. My 2045 fund from Vanguard has returned 5.70% annually over the past 10 years. Not half bad, but pales against the 7.39% for the Vanguard 500 over the same time period. Meanwhile, the 2010 fund (closed, obviously) has returned 4.68% over the same time period.

- Allocations may not match your wishes. Just because someone somewhere stated that this was the best allocation for you, doesn’t mean that they’re right. What if you want to be more (or less) aggressive? Out of luck.

Results

Target date funds are a “good” option for most people. You certainly won’t lose your shirt with a target date fund. If you have no time, or little money, but need to park your money somewhere, you could do much worse than a target date fund.

That said, I don’t use target date funds, and have none of them in my portfolio; they are much too conservative for me. Given what I believe we are going to need to retire, I think they are much too conservative for anyone who isn’t very close to retirement.

The difference between 6% return and 8% return over a working life time is quite significant, and can be hundreds of thousands of dollars, depending on how much you have saved up.

When I retire or get close to it, the calculation will be different, of course. I’ll very likely change to something more conservative. But at that point, I won’t need a target date fund for that.

But if ready to invest, and you’re indecisive, and you’re overwhelmed with options, don’t think too hard about it. If a target date fund feels like the easiest option, go for it.

But maybe revisit it at some point.

But enough about me. What do you think about target date funds?