I’ve always believed that in business you can compete on price or you can compete on quality, but never both. Which is why we have basic economy on airplanes (which are as cheap as possible and as a consequence are as painful as possible), and The Residence on Etihad Airways, a three-room suite for a single person (living room, bedroom, and en suite shower room, on a plane).

But sometimes a race to the bottom isn’t a bad thing. When the quality of a product isn’t up for alteration, when everyone is selling more or less the same thing, you can afford to be discriminating on price.

Mutual fund companies such as Vanguard and Fidelity know this. Ever since 40 years ago when Vanguard came out with the first “index fund” (a low-cost mutual fund that aims to passively track an index, with no magic powers of a broker needed) the fees that people pay to own mutual funds have been on a downward trajectory.

For example, since 1996, a year which I could find figures on, the average fee for an equity mutual fund was 1.04%, and as of 2017 it was 0.59%. A 0.63% difference may not seem like a lot, but it’s a difference that can certainly add up over the years.

Vanguard’s mutual funds have typically had two tiers, a standard (“Investor”) tier, with a lower minimum balance (usually $3,000), and a higher (“Admiral”) tier, with a higher minimum balance (usually $10,000). The theory being that the more money you invest, the lower your cost.

But recently, Vanguard has been getting competition from other firms, specifically Fidelity, which recently announced a 0.00% fee on some of its mutual funds. So perhaps in response, they just announced a change: For a few dozen of its most popular funds, now everyone gets access to Admiral Shares, even with only a $3,000 minimum balance.

This is great, and falls into the category of “free money”.

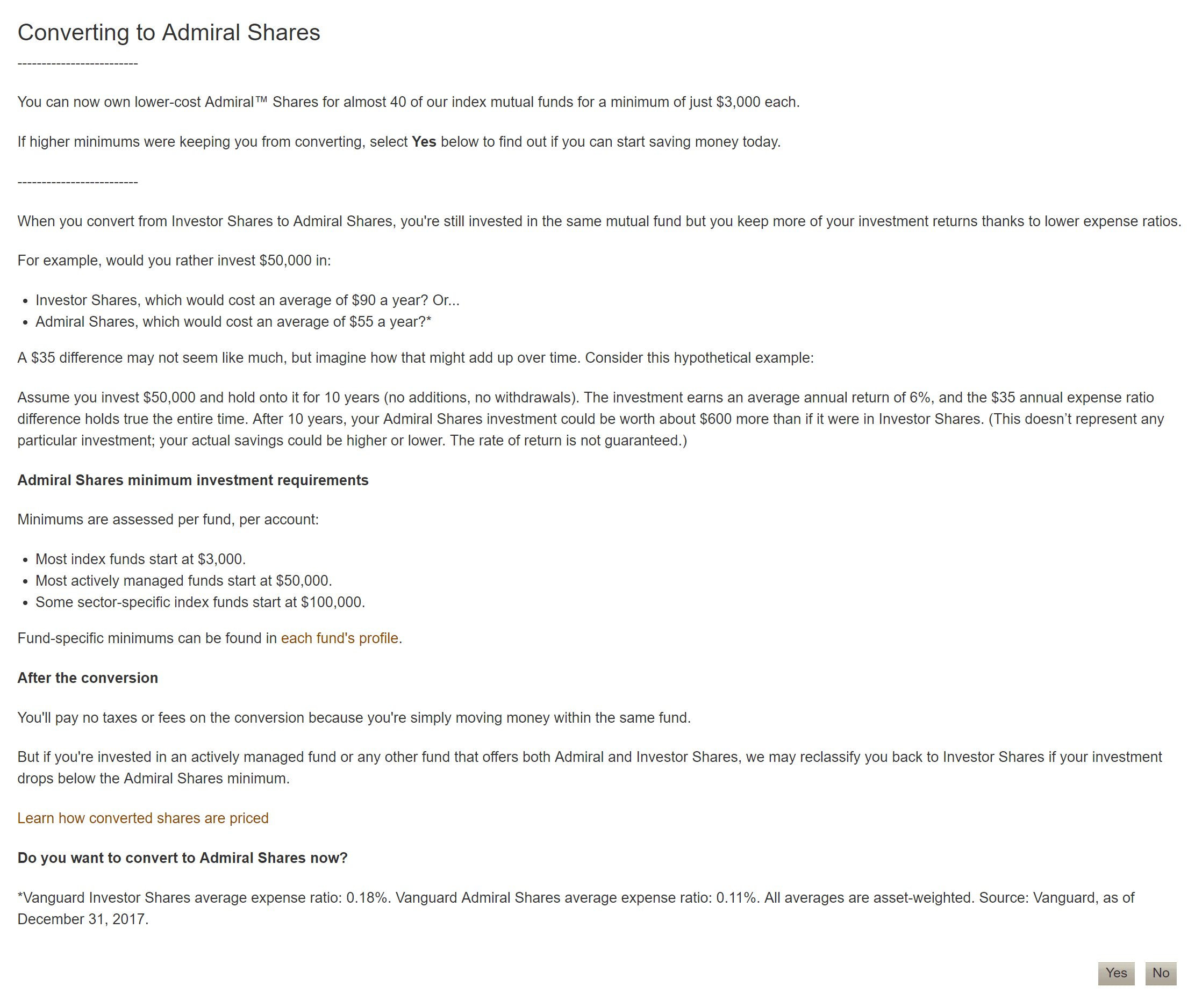

I received this email recently:

For example, the Vanguard 500 index fund, when bought as Investor Shares ($3,000 minimum), has a fee of 0.14%, which is quite low. To make it easier, think $0.14 paid per year per $1,000 invested. Peanuts.

But for Admiral Shares, the Vanguard 500 has a fee of only $0.04%. Which makes peanuts look like cannonballs.

So I logged in, and sure enough, on the accounts I have that have funds where I had less than $10,000, I saw a note:

Clicking the prompt brings up one of the most hilariously bad, text-laden wizards.

From there, each applicable mutual fund will be listed. Select one to convert it.

(Actually, it’s pretty annoying, because if you have multiple funds, you have to go through this wizard multiple times. But then again, we don’t use Vanguard for the website, we use it for the returns on investment, right?)

So what do you need to do?

Nothing technically. If you have eligible Vanguard shares, Vanguard will automatically convert your shares to the lower cost versions, “over the next year”.

But why wait? It’s super easy. Just log on to your Vanguard account, find the link the looks like the above, and follow the prompts.

Not sure if your funds are eligible? Here is a list.

I’m usually a skeptic for these types of “we’re giving you free money” type deals, but I was unable to find a downside to this. I think this really is just a product of the market getting more competitive.

Now, for many mutual funds, the fee that we’ve been talking about, the “expense ratio”, isn’t the only charge that gets passed to customers. There are load charges, 12b-1 fees, and a lot of other alphabet soup that are designed to confuse you.

So it’s always important to know what fees you’re paying.

But at least for many Vanguard mutual funds, these particular fees are getting lower.