I discuss the new upcoming rules for student loan repayment, including the new Repayment Assistance Plan (RAP).

I always loved the YouTube series: “Epic Rap Battles of History“. These would pit two famous historical characters against each other, taking turns rapping at each other on why they are better than the other. My personal favorite is Albert Einstein versus Stephen Hawking:

Well, I wish right now we’d have a new one, starring this administration’s Department of Education versus the 43 million people trying their damnedest to pay off their student loans.

Now that would be an epic rap battle. Unfortunately, borrowers have a real RAP battle on their hands in the form of a new landscape of repayment terms.

Strap in, as everything is about to change yet again.

The situation so far

I’ve long written about the “alphabet soup” of income-based repayment plans that student loan borrowers have had to contend with. Plans like “PAYE”, “ICR”, “SAVE”, etc. The eligibility, terms, and details were all different, but often not so terribly different.

To help with this, the Department of Education has hosted a page called the “Loan Simulator“, which allowed you to input your loan situation and then see all of the different plans and options. It was kind of the only way to figure out the best deal for your situation.

Even the phrase “best deal” can mean different things to different people. Is the goal to pay off your loans as fast as possible? Pay as little as possible? Work toward loan forgiveness as fast as possible? It’s very confusing.

Now, previous Departments of Education have been sympathetic, even supportive in helping borrowers get the best deal possible. The Biden Administration created the SAVE plan which allowed for lower monthly payments with an aggressive 20-25 year forgiveness timeline.

Today’s Department of Education appears to have one driving motto: “Give me back my money.”

And with this, a new repayment plan was born.

Enter RAP

Legislation in 2025 created a new repayment plan called Repayment Assistance Plan, or RAP. One of the goals with this was to simplify the repayment options for borrowers.

So as the RAP plan comes into effect, the following plans are going to be discontinued:

- ICR

- PAYE

- SAVE

So in effect you will eventually have two options: standard repayment and RAP.

And this all goes into effect on July 1, 2026. If you have loans disbursed after this date, they will be eligible for RAP only if anything at all.

How does RAP work?

Here are the main bullet points for RAP:

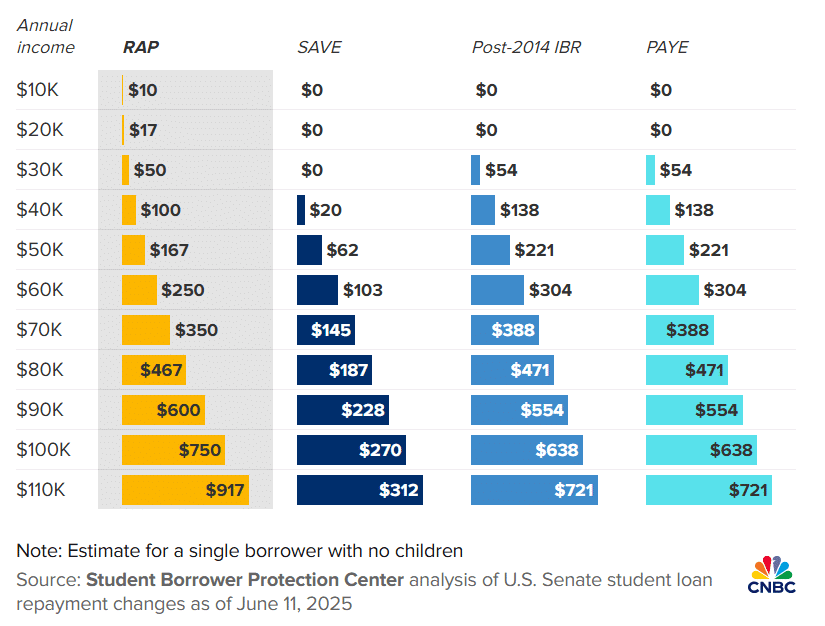

- Payments are based on your Adjusted Gross Income (AGI) from your tax return, ranging between 1-10%, depending on your income. (Here’s a chart.) Previously the calculation was based on “discretionary income”, which ended up being more favorable to borrowers.

- Loan forgiveness happens at 30 years. (And you will need to pay taxes on the forgiven amount.)

- The loan balance will never grow; if your payment doesn’t cover the interest, the extra interest is waived

- Borrowers will always have to pay something each month, regardless of income.

Benefits and drawbacks of RAP

RAP is a mixed bag. On one hand, there are some definite benefits:

- Simplicity. You now have two options: Standard repayment or RAP. No more alphabet soup.

- Your balance can’t grow. No more situations where people pay for years and years only to have a larger balance than when they started.

- Loan forgiveness. It’s still on the table.

- Compatible with PSLF. Those in the Public Service Loan Forgiveness program (which isn’t going away) can be on RAP and still potentially get loans forgiven after 10 years.

But there are some serious drawbacks:

- You will pay more. According to CNBC, you will almost certainly be paying more than you would have on previous repayment plans.

- Loan forgiveness comes later. Older plans offered forgiveness at 20-25 years. Now it’s 30.

What about preexisting loans?

If you already have loans in plans such as ICR or PAYE, the loans may remain in those plans for 2 years. After June 30, 2028, they will be automatically moved to the standard plan unless you choose RAP.

With SAVE, it’s a little different, in that you may have 90 days to pick another plan. Because of this, you could potentially switch from SAVE to ICR or PAYE for the remainder of this two year period, and then switch over to RAP.

It’s hard to say whether that’s worth it though, as it depends on your specific situation. The simplest option is to switch to RAP now, though, if you can afford it.

What to do now

If you are enrolled in a current income-based repayment plan, don’t ignore these changes. You have to pick a new plan and get on it before the deadline passes. Failure to do this will mean that you get moved on to the standard repayment plan, which might be a drastic increase in your monthly bill. (And plus, no loan forgiveness option.)

If you do nothing else, log on to your account at StudentAid.gov and check up on your current borrowing situation. See what plan you’re on, and what you’re paying (in case you’ve forgotten). You can also manage the change in plan right in your account. That’s right, you can sign up for RAP online.

And if you don’t want to make any changes now, set a calendar reminder for 90 days from July 1st (if you’re on the SAVE plan) and for two years (if you’re on another plan). You’ll not want to let this deadline pass you by.

Not the final battle

We’ve seen the student loan repayment situation change drastically in just a few years, from the diminished payments of SAVE to the new larger payments of RAP.

That tells me one thing: this isn’t the final say.

I fully expect more changes to come with student loans in the near future, certainly within the next 5 years. This is why it’s important to not ignore what’s going on with the changes, as it’s your money at stake here.

And it’s most important to always continue to pay your bills on time and in full every month. Student loans are a major hassle and a huge drain on your ability to build wealth, but I can assure you that not paying them will be even worse.

Stay patient. The RAP battle isn’t over yet.

What are you going to do about your student loans?