Sales of new cars are sluggish amidst higher prices and economic uncertainty. But maybe it isn’t a problem if you can’t afford a new car.

I love watching old commercials. Car commercials can be especially fun.

Take the first one in this compilation:

It’s for a 1992 Pontiac Grand Prix , and it boasts such features as: Air conditioning! AM/FM stereo cassette! 4-speed automatic! Power windows! Power door locks!

And for all of these incredible features were available to the buyer for a 48 month “smartlease” of $264 a month.

Now, leases weren’t a good deal then, and they aren’t a good deal now. But what’s interesting to me is that this random data point that I was going to use to show how much worse things have gotten for new car buyers is actually kind of showing me the opposite.

Here’s the headline: new car sales are trending downward, and the conventional wisdom says that it’s because prices (and interest rates) are too high.

I’d argue that this isn’t necessarily a bad thing. But it turns out that this might not actually be so true in the first place.

Table of Contents

The current crisis

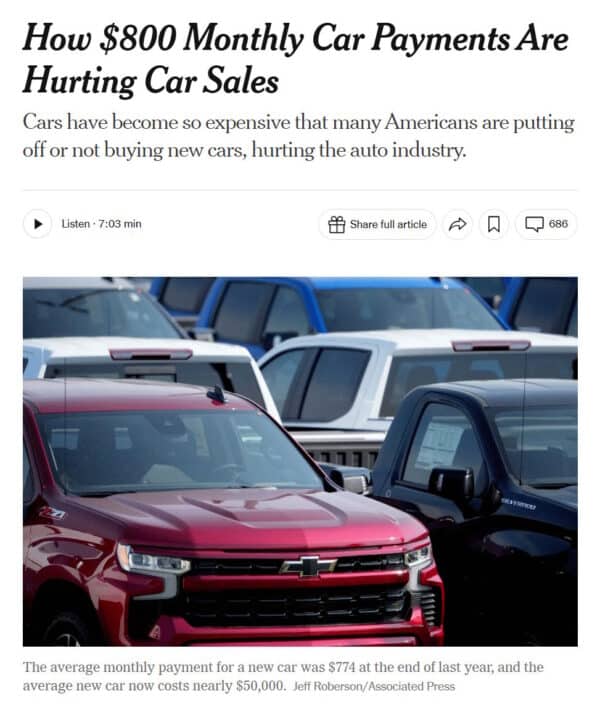

There’s a recent New York Times article about the cost of new cars:

The gist of the article is that new cars have become too expensive, both the sticker price and the interest rate:

The average interest rate on a 60-month new car loan from banks was 7.22 percent in November, according to the Federal Reserve. While that is down a little from early 2025, it is still much higher than in 2021 when the rate averaged 4.8 percent. Add to that the average price of new cars has reached nearly $50,000, up from $38,400 in 2019.

The article mentions tariffs and the ongoing geopolitical situation as reasons for the increases.

“It’s not an exaggeration to say this is a crisis,” said Taz Harvey, the owner of Honda, Mazda and Chevrolet dealerships in central California.

The car price crisis

Look at this quote:

Maybe it was the recession and the uncertainty over the economic well-being of the nation that kept consumers from buying new cars last year. Maybe some of the blame for the auto sales downturn should focus on the window sticker. Maybe people aren’t buying as many cars as they used to because they can`t afford cars like they used to.

This quote is from an article from 1992. So I’m not sure that what we’re dealing with is entirely new.

New car prices in 1992

Let’s keep going with the 1992 statistics, as I happen to have them here.

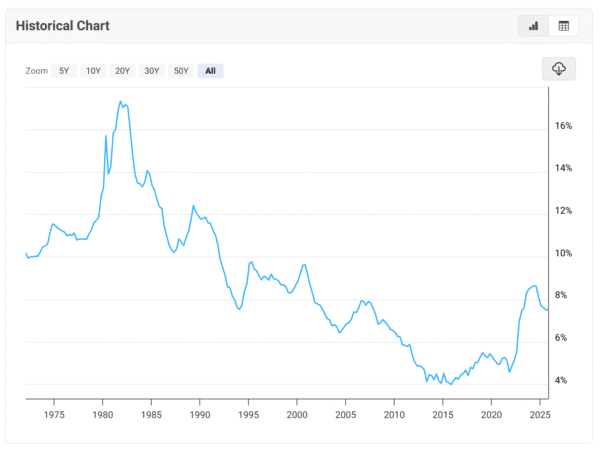

Interest rates on a 48-month car loan was roughly 9% in 1992, compared to 7.5 now. So that’s lower now.

But, the cost of a new car in 1992 was approximately $16,300, or about $38,000 in today’s money. Today it’s $49,000.

So that seems like a wash to me.

But people today aren’t comparing the interest rates to 1992. They’re comparing interest rates to a few years ago, when they were near zero. From the article at the top again:

“The last time I bought, I got 0.9 percent, so if it’s 5 this time, it’s a no.”

Which is the anomaly?

The data appears mixed to me. That 1992 Pontiac Grand Prix would have cost a little over $630 a month in today’s dollars, which isn’t too different from an equivalent car payment today.

In fact, at least one source argues that the price of an equivalent car has actually gone down over the past decade, and by a considerable 9%! The article argues that cars are more expensive because people are buying larger cars, which does track.

And as for interest rates, are the interest rates we’re dealing with now high, or did we just come out of a few years of abnormally low interest rates?

Source: Macrotrends

I’m just saying, I don’t quite believe the narrative that new cars are uniformly more expensive now.

Should we care?

That said, let’s say that the narrative is true, and that cars are, on the whole more expensive across the board.

Should we care? I’m not so sure.

As I’ve written about many times, buying a new car is, for most people, a terrible financial decision.

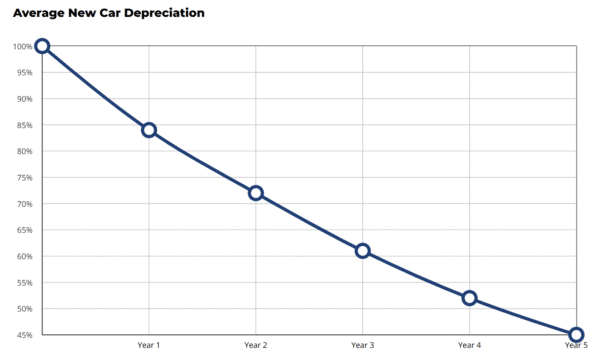

A new car loses a big chunk of its value—somewhere between 10-20% in its first year. depending on the source—the second its bought.

A $50,000 car, then, loses $5,000-$10,000. Do you have that much money to burn?

Kelley Blue Book notes a greater than 50% drop in value over the first five years of a car’s life.

Now, it’s not the 1990s anymore. Cars last a long time. You can get up to 200,000 miles on most cars easily, and 15 years isn’t a long time for a car to last.

So if you were to buy a five year old car today, you’d get it for less than half the price of new, and could probably keep it for at least a decade.

This can save you tens of thousands of dollars. I’ve argued that keeping my first car running for years after people said to junk it was the primary reason I was able to afford to buy a home.

Will used cars become more expensive too?

So will this supposed price increase of new cars trickle down to the used market?

No idea, unfortunately. I imagine it’s all a matter of supply and demand in the marketplace.

But what I can say is that if you’re buying the five year old car (at 45% of its new-car value), you’re going to be impacted a lot less.

And also, there’s also the future prospect of cheaper cars from China eventually making their way onto U.S. roads. I was in Mexico recently and saw my first BYD car; it’s only a matter of time before they come here. And when you can buy an EV car for under $20,000, everything is going to change.

Your task: Start saving now

Cut through the noise, and you see a few truths that have nothing to do with the current prices: You will likely be buying a different car in a few years, so start saving up money for this inevitable purchase now. If you’re stuck in a car loan, then wait until you pay off the car loan, and then put that money toward the next car.

Because you know how you can save thousands of dollars on a car? Buying it without a car loan. And that’s true no matter what the price of a car is.